by Tom Konrad, Ph.D., CFA

The last three months of 2020 brought an explosion in clean energy stock prices.

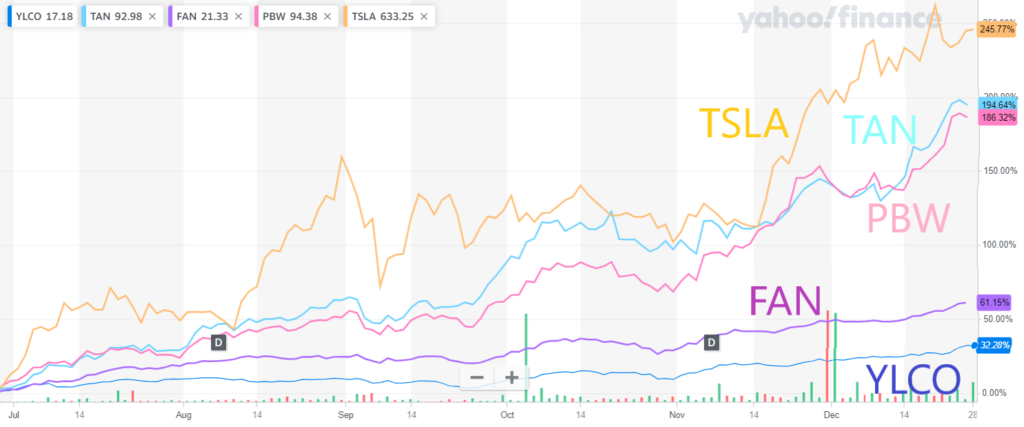

Solar stocks (as measured by the Invesco Solar ETF (TAN), nearly tripled. So did the Invesco Wilderhill Clean Energy ETF (PBW), which includes a broader spectrum of companies. Wind stock rose 61%, and even the relatively sedate Yieldcos were up 32%. The stars of the last half of 2020 was undoubtedly Tesla (TSLA, up 246%) and other electric vehicle stocks.

Money Flows Out of Fossil Fuels and Into Clean Energy

I believe that the cause of the current rise in stock prices is largely the fossil fuel divestment movement, which gained significant momentum in 2020. Not only have I been hearing greater interest in divestment from individuals, but major money managers like Blackrock and the New York State Pension Fund have stated their plans to divest from fossil fuels over time. If you have not already taken your money out of fossil fuel stocks, you are late to the game. As I wrote in 2014, when it comes to divestment, the last one out loses.

The same goes for investing in clean energy stocks. While not all the money taken out of fossil fuel stocks flows into clean energy stocks, some of it does. The market capitalization of clean energy stocks is quite small compared to the amount of money flowing into the sector: Demand for shares in clean energy companies is rising faster than companies are going public or issuing new shares.

Issuing New Shares

Economics 101 tells us that when demand increases faster than supply, the price rises. This is exactly what we have seen in clean energy stocks in the second half of 2020. We also learned that when price rises, it induces increased supply: More clean energy companies will go public and/or issue new shares.

Rising stock prices bring more than just stock market profits, they are also significant for the companies. Companies will refrain from raising money in secondary offerings unless they are confident that the offering will be “non-dilutive.” A non-dilutive share offering is one in which the money will be invested in a way that increases earnings more as a percentage than the number of shares is increased. This allows the offering to have the effect of increasing future earnings per share, despite the increase in the number of shares.

As a company’s stock price rises, more potential investments become non-dilutive, and investments that are already non-dilutive become even more attractive. The company’s private competitors will also benefit. They will find it easier to raise money from investors who use the valuations of publicly listed firms to determine what the firm is worth.

If clean energy stock prices stay at their current level for a few months, we will see increasing numbers of companies going public through IPOs and Special Purpose Acquisition Companies (SPACs). We will also see more established companies raising money through secondary offerings.

The Gold Rush

As I learned when I took California History in elementary school, the most reliable way to make money in the state’s 1849 gold rush was to sell picks and shovels to aspiring gold miners. Three of the stocks in my Ten Clean Energy Stocks for 2021 model portfolio are metaphorical picks and shovel suppliers to clean energy industries.

If Tesla’s stock price rise is any guide, there will be significant new investment flowing into manufacturing electric vehicles. Autoparts manufacturer Valeo, SA (FR.PA, VLEEF, VLEEY) specializes in vehicle electrification, autonomous driving, and comfort systems, so it’s clearly well positioned to help automakers focus more on Tesla’s specialties: Electric and autonomous driving.

Global water, energy, and waste management giant Veolia (VIE.PA, VEOEF, VEOEY) is also firmly in the picks and shovels business, although their clients are more often large multinational companies and municipalities rather than clean energy firms. Yet Veolia is a potential beneficiary from the boom in clean energy stocks. They own and develop clean energy and recycling projects which could potentially be sold when acquisitive clean energy companies start bidding up the prices of clean energy projects. They also have access to valuable urban real estate at their municipal utilities where they could develop solar and wind projects for sale to clean energy firms with money to spend.

Umicore, SA (UMI.BR, UMICF, UMICY) is also well positioned for the boom in electric vehicles. It produces cathode materials for lithium-ion batteries, and is a battery recycler. The electric vehicle boom is currently constrained by the supply of lithium-ion batteries and the supply of specialty metals (lithium, manganese, cobalt and nickel) that go into their manufacture. The mining of many of these materials often takes place under exploitative and environmentally harmful conditions in poor countries. Although still a small portion of the battery materials market, Umicore’s recycled materials can claim a price premium based on battery manufacturer commitments to ethically sourced raw materials. Although still in their infancy, recycled content mandates like the one Europe recently passed will also play a role.

Finally, dry bulk shipping firm Scorpio Bulkers, Inc. (SALT) is repositioning itself to sell picks and shovels to the burgeoning offshore wind industry. Dry bulk shippers carry bulk unpackaged cargoes like ore, grains, coal, and metals. Scorpio is selling its dry bulk shipping fleet and using the proceeds to buy offshore wind turbine installation vessels. In addition, it is applying to change its name to better reflect its future business.

While SALT’s first wind turbine installation vessel is unlikely to be delivered until 2023, I believe that the rebranding will allow the company to attract part of the flood of cash pouring into the clean energy space.

It is also value priced. The company had 11.5 million shares outstanding, $1,429 million in assets, and $675 million in liabilities at the end of September 2020. It expects to write down the market value of its vessels by between $475 million and $500 million to reflect their true market value. That market value is also the price at which they are currently being sold. It has made nine announcements of ship sales since mid-November. Since the sales are ongoing, we can expect its write-down estimates to be reasonably accurate. After the sale of its vessels, its main assets will be easy-to-value cash and contracts to buy wind turbine installation vessels. After subtracting liabilities, Scorpio will be worth approximately $254 million to $279 million, or $22 to $24 per share. The stock is currently trading in the $17 to $18 range.

Conclusion

Unless it suddenly reverses, the recent run-up in clean energy stock prices is likely to lead to a real-world investment boom in clean energy. While undoubtedly necessary to accelerate the world’s transition away from fossil fuels, not all such investments will be profitable, especially when they amount to buying other clean energy companies at also inflated prices.

During an investment boom, the companies selling tools and supplies to the investors are often more profitable than the investments themselves. That’s what I hope for Valeo, Umicore, and Scorpio Bulkers (under a new name that highlights its new business) in 2021.

DISCLOSURE: Long VLEEF, UMICF, SALT, VEOEF

DISCLAIMER: Past performance is not a guarantee or a reliable indicator of future results. This article contains the current opinions of the author and such opinions are subject to change without notice. This article has been distributed for informational purposes only. Forecasts, estimates, and certain information contained herein should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed.

{kind=link}