by Tom Konrad Ph.D., CFA

Will shareholders accept the deal?

On Monday, 8point3 Energy Partners, the joint YieldCo from First Solar and SunPower, entered into a definitive agreement to be acquired by Capital Dynamics.

When public companies are sold, it’s almost always at a premium to the market price. It’s that price premium that persuades shareholders to sell. So why would 8point3 (NASD: CAFD) shareholders accept a deal that offers them only $12.35, or 15 to 20 percent below the roughly $15 price CAFD has been trading around for the past three months?

To answer this question, we need a little history.

Jan Schalkwijk, founder and portfolio manager at investment advisory firm JPS Global Investments, said that First Solar (NASD: FSLR) created 8point3 to unlock capital for its solar project development business.

“First Solar got into the solar project business as a means to pull demand for its panels in an over-supplied market,” said Schalkwijk. “As it turns out, First Solar was quite good at it, and many of the largest utility-scale solar plants in operation in the U.S. today are First Solar projects.”

“But operating a solar plant is inherently a different business from producing solar panels and locks up a lot of capital,” Schalkwijk added. “Also the investment thesis is different and more yield-driven than the higher risk (and higher cost of capital) product side. To free up capital and reduce the cost of capital for projects to pencil out, it formed a YieldCo, 8point3.”

He expects that SunPower’s reasons were similar.

From the point of view of solar manufacturers like First Solar and SunPower, the reason to own a YieldCo is to have a captive buyer of solar projects. Since that YieldCo could not raise money in the stock market to buy projects at attractive prices, they chose to sell the YieldCo itself.

JPS Global holds First Solar and a small position in SunPower in client accounts. They sold all holdings of 8point3 in 2017. JPS is also the manager of the Green Income Folio strategy. I am the primary research provider and joint developer of this strategy, which includes First Solar on Schalkwijk’s recommendation, but no position in CAFD.

An offer they can’t refuse

The argument for shareholders to approve the buyout amounts to: “Not the best YieldCo you got there. Shame if no one were to buy it.”

The long-term prospects for 8point3 as a standalone company are not bright. This has been apparent for some time, but the price has been going up anyway. I believe that the recent stock price strength (which has eroded since the sale was announced) arises out of mostly small investors focusing only on the current dividend without any consideration of its sustainability, while the more sophisticated investors are reluctant or unable to short the stock. Recent news headlines (like this and this) support this point.

Obviously, 8point3’s stock was risky, something I and most professional investment analysts have been pointing out for the last year. According to Yahoo, eight out of 11 analysts rated 8point3 a “Hold” or “Underperform” at the start of the month.

I personally wrote an article on Greentech Media last July, which attempted to value the YieldCo in the case of a sale. Looking at the long-term sustainability of 8point3’s cash flow, I came up with a valuation range of $8 to $13, which puts the actual offer at the high end of my range.

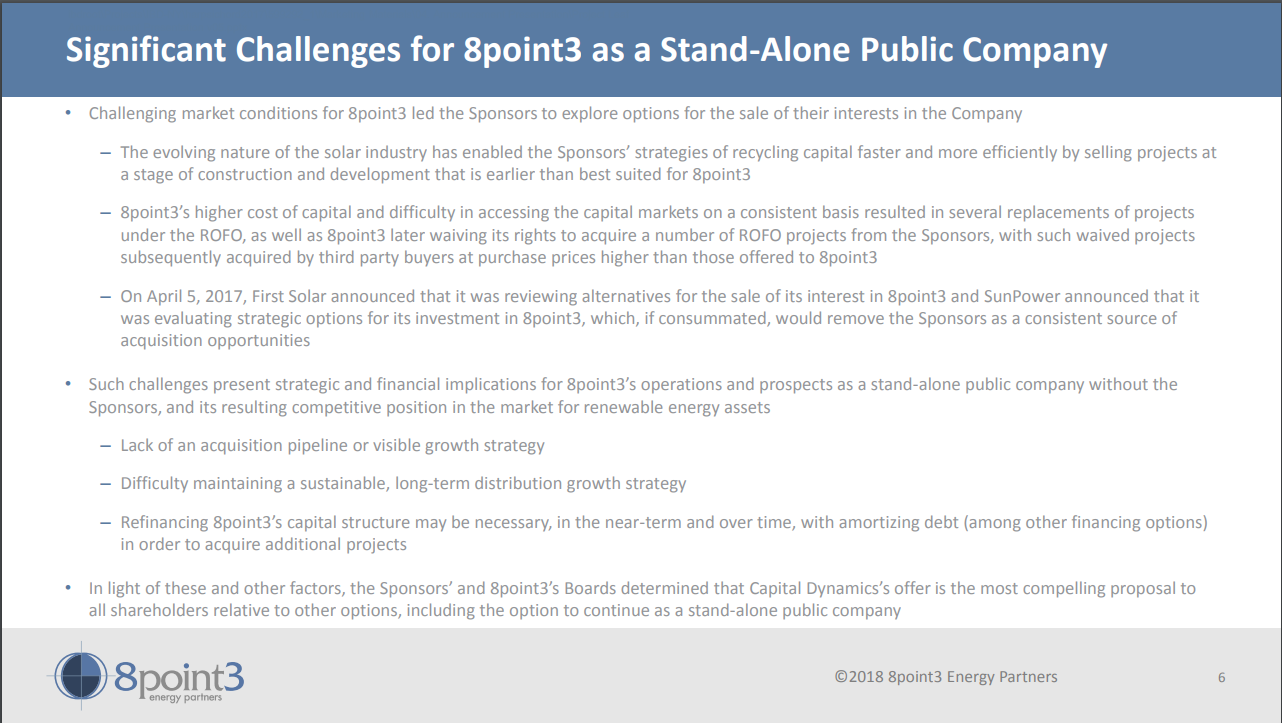

Significant challenges for 8point3 as a standalone public company

An investor presentation on the sale of 8point3 outlines the risks to the YieldCo’s business model, while trying to shift the blame for the company’s perilous condition onto “market conditions.” These are the same risks that professional analysts have been highlighting, but which small investors seem to have ignored.

What 8point3 wrote: “The evolving nature of the solar industry has enabled the Sponsors’ strategies of recycling capital faster and more efficiently by selling projects at a stage of construction and development that is earlier than best suited for 8point3.”

Translation: The 2017 downturn in solar installation meant that First Solar and SunPower need to sell solar farms quickly, often before they are completed. YieldCos like 8point3 typically buy solar farms after completion.

What 8point3 wrote: “8point3’s higher cost of capital and difficulty in accessing the capital markets on a consistent basis resulted in several replacements of projects under the [right of first offer], as well as 8point3 later waiving its rights to acquire a number of ROFO projects from the Sponsors, with such waived projects subsequently acquired by third-party buyers at purchase prices higher than those offered to 8point3.”

Translation: 8point3’s stock price is not trading at a large enough premium for it to sell shares to investors and invest in new solar farms while increasing the dividend. In short, investors are not willing to pay more for 8point3 shares than its current projects are worth. Unless First Solar and SunPower can sell projects to 8point3 at attractive prices, they have no reason to own it.

What 8point3 wrote: “Such challenges present strategic and financial implications for 8point3’s operations and prospects as a standalone public company without the Sponsors, and its resulting competitive position in the market for renewable energy assets:

- Lack of an acquisition pipeline or visible growth strategy

- Difficulty maintaining a sustainable, long-term distribution growth strategy

- Refinancing 8point3’s capital structure may be necessary, in the near-term and over time, with amortizing debt (among other financing options) in order to acquire additional projects.”

Translation:

- 8point3 can’t grow in current market conditions

- Our dividend growth is unsustainable

- We have to refinance debt before 2020, and that would require a dividend cut

What 8point3 wrote: “In light of these and other factors, the Sponsors’ and 8point3’s Boards determined that Capital Dynamics’ offer is the most compelling proposal to all shareholders relative to other options, including the option to continue as a stand-alone public company.”

Translation: If shareholders reject this offer, they’ll regret it.

All of these risks have been clear to analysts (if not the investing public) since 8point3 started looking into refinancing its debt a year ago. What’s truly groundbreaking here is that these arguments are now being put forward by a YieldCo and its sponsors.

In 2017, 8point3 gave guidance for the year on the January 26, 2016 fourth-quarter conference call. It now looks like they delayed the 2017 fourth-quarter call in anticipation of this announcement. My 2017 analysis indicated that, without further acquisitions, 8point3 would likely see a slight decline in 2018 cash available for distribution.

Now that this deal has been announced, management has an incentive to release the bad news. I think we can expect plenty in the Q4 conference call, which, in turn, should get shareholders to vote for the deal.

The big picture

While many YieldCos have struggled since the popping of the 2015 YieldCo bubble, the discounted purchase price for 8point3 stock points more to specific problems at one company, rather than the YieldCo space in general.

On February 7, as this article was being written, NRG Energy (NYSE:NRG) announced the sale of its ownership stake in its YieldCo NRG Yield (NYSE:NYLD and NYLD/A) and its renewables development business and projects to global infrastructure investor Global Infrastructure Partners (GIP). On the same day, TerraForm Power (NASD:TERP) made an offer for Spanish YieldCo Saeta Yield (Madrid: SAY) at a 20 percent premium to the recent market price.

In contrast to the 8point3 sale, NRG Yield’s public shares are not being purchased. GIP will continue as a new sponsor of the public YieldCo, and is committed to NRG Yield’s future growth. In a press release, Adebayo Ogunlesi, chairman and managing partner of GIP, said, “We are…excited about the opportunity to grow the value of NYLD, which allows public market investors to access attractive investments in renewable energy.”

This echoes the sentiments of Brookfield Asset Management (NYSE:BAM) and Algonquin Power and Utilities (NYSE:AQN) in their recent purchase of sponsorship stakes in TerraForm Power and Atlantica Yield (NASD:AY) when those YieldCos’ respective sponsors filed for bankruptcy.

Most recent YieldCo sales have been a result of problems at the former sponsors, while 8point3’s sale is more a product of problems at the YieldCo itself. This is why 8point3’s shareholders are faced with selling at a discount, while shareholders of TerraForm Power and Saeta Yield received and/or are being offered a premium.

Stay tuned for a more in-depth analysis of the four recent YieldCo transactions and the state of the YieldCo space in general.

***

This article was first published on GreenTech Media.

Disclosure: Long TERP, AY, NYLD, NYLD/A, AQN. Short calls on CAFD. Short puts on FSLR (an effective long position). Tom Konrad and Jan Schalkwijk have an affiliation with the Green Income Folio, which is long TERP, AY, NYLD, NYLD/A and FSLR.

{kind=link}